Français

Français  Deutsch

Deutsch  Español

Español  Italiano

Italiano  Nederlands

Nederlands  Português

Português  Brasileiro

Brasileiro  Ελληνικά

Ελληνικά  Polski

Polski  Română

Română  Svenska

Svenska  Türkçe

Türkçe  Български

Български  हिंदी

हिंदी

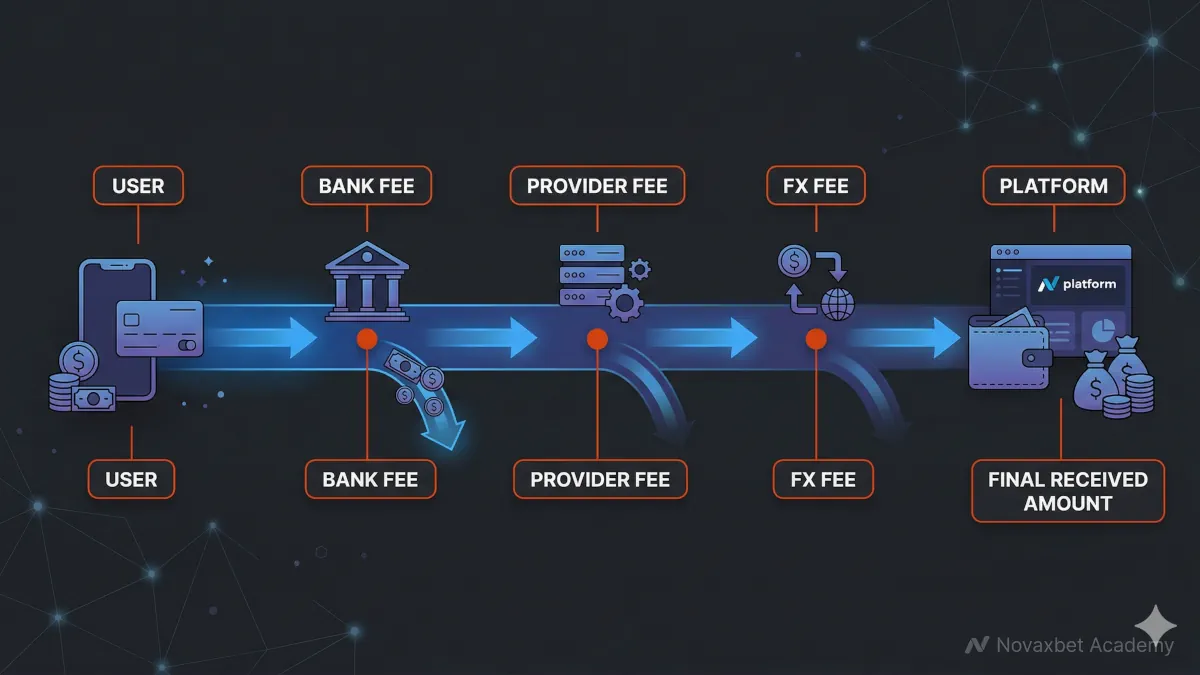

Fees in Bank Transfers

Understanding the different types of fees involved in bank transfers.

Novaxbet Editorial •2026-05-16•3 min read

Instant bank transfers are designed for speed and efficiency, but they are also subject to various limits and restrictions. These controls are necessary to manage risk, comply with regulations, and ensure system stability.

Understanding these limits helps users avoid failed transactions and plan payments effectively.

Do Instant Bank Transfers Have Limits

Next reading

Yes, instant bank transfers have limits.

These limits can apply to:

- transaction amount

- daily or monthly totals

- number of transactions

Limits vary depending on the bank, platform, and payment system.

Types of Limits

Different types of restrictions may apply.

Per Transaction Limits

Maximum amount allowed per single transfer.

Daily Limits

Total amount allowed per day.

Monthly Limits

Aggregate limits over longer periods.

Frequency Limits

Restrictions on how often transfers can be made.

Each type controls a different aspect of usage.

Bank-Imposed Limits

Banks set limits to manage:

- fraud risk

- liquidity

- operational capacity

These limits may differ between accounts and users.

Payment Network Limits

Payment systems also impose restrictions.

Examples include:

- SEPA Instant caps

- real-time payment network thresholds

These limits apply regardless of the bank.

Platform-Level Limits

Payment platforms may define additional rules.

They may limit:

- deposit amounts

- withdrawal sizes

- transaction frequency

Platform limits can be stricter than bank limits.

Regulatory Restrictions

Regulations can influence limits.

These may include:

- anti-money laundering (AML) rules

- transaction monitoring requirements

- jurisdiction-specific caps

Compliance affects how payments are processed.

Limits Based on User Profile

Limits may vary depending on:

- account verification level

- transaction history

- geographic location

Higher verification often increases limits.

Currency and Regional Limits

Limits can differ by:

- currency

- country

- payment scheme

Not all regions support the same thresholds.

Why Limits Exist

Limits are designed to:

- reduce fraud risk

- protect users

- ensure system stability

They are essential for secure operations.

What Happens When a Limit Is Reached

If a limit is exceeded:

- the transaction may be declined

- the user may be asked to reduce the amount

- alternative payment methods may be required

Understanding limits helps avoid disruption.

Increasing Transfer Limits

In some cases, limits can be increased.

This may involve:

- completing identity verification

- upgrading account status

- contacting the bank or provider

Not all limits are adjustable.

Instant vs Traditional Limits

Limits may differ between systems.

Instant transfers:

- often have lower maximum limits

- prioritize speed and risk control

Traditional transfers:

- may allow higher amounts

- involve longer processing times

Users must choose based on needs.

Limits and Security

Limits contribute to security.

They:

- reduce exposure to large losses

- control transaction behavior

- support fraud detection systems

Limits are part of risk management.

Planning Around Limits

Users can manage limits by:

- splitting large payments

- scheduling transactions

- using alternative methods

Planning reduces friction.

Limits vs Flexibility

Instead of thinking:

“Limits are restrictive”

A better perspective is:

“Limits balance usability, safety, and system reliability”

They ensure the system works effectively for everyone.