Français

Français  Deutsch

Deutsch  Español

Español  Italiano

Italiano  Nederlands

Nederlands  Português

Português  Brasileiro

Brasileiro  Ελληνικά

Ελληνικά  Polski

Polski  Română

Română  Svenska

Svenska  Türkçe

Türkçe  Български

Български  हिंदी

हिंदी

What Is Slippage on a Betting Exchange?

Understanding price slippage and how order execution differs from expected odds.

Novaxbet Editorial •2026-03-02•5 min read

When placing a bet on a betting exchange, many participants assume their order will be executed exactly at the price displayed on screen. In reality, execution depends on available liquidity at that precise moment.

Slippage occurs when the final matched odds differ from the expected odds at the time the order was placed.

This difference is not an error or malfunction. It is a natural consequence of how exchange markets operate.

Unlike traditional bookmakers, exchanges match orders between participants rather than guaranteeing prices.

Execution therefore depends on market depth, order timing, and competing activity.

How Slippage Happens

Next reading

Every betting exchange operates through an order book containing available back and lay offers at multiple price levels.

When an order enters the market, it consumes available liquidity starting from the best available price.

If sufficient liquidity does not exist at that price, the remaining portion of the order continues matching at worse prices.

This process creates slippage.

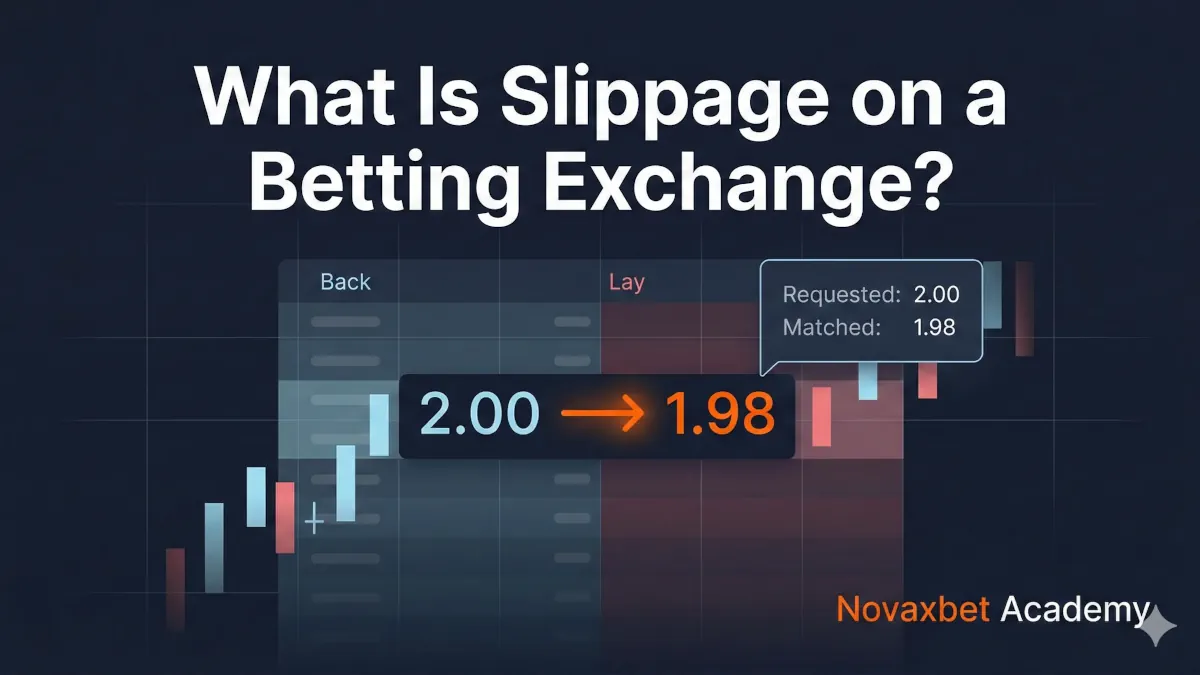

Example

Suppose the market shows:

- Back price: 2.00

- Available liquidity: €500

A participant submits a back order for €1,000.

Execution occurs as follows:

- €500 matched at 2.00

- Remaining €500 matched at 1.98

Final average matched price becomes lower than expected.

The trader experiences negative slippage.

Positive vs Negative Slippage

Slippage does not always work against the participant.

Negative Slippage

Occurs when execution happens at worse odds than requested.

Example:

- Intended back at 2.00

- Actual average execution at 1.98

Higher cost of entry.

Positive Slippage

Occurs when execution happens at better odds.

Example:

- Intended lay at 2.00

- Execution matched partially at 2.02

Improved pricing outcome.

Exchange markets allow both outcomes because prices continuously move during matching.

Market Orders vs Price-Controlled Orders

The probability of slippage depends heavily on order type.

Aggressive (Market-Taking) Orders

Orders that immediately accept available prices.

Characteristics:

- Instant execution

- Higher slippage risk

- Liquidity consumption

Used when speed matters more than price precision.

Passive (Limit) Orders

Orders placed at a specific price waiting to be matched.

Characteristics:

- Controlled pricing

- Lower slippage risk

- Uncertain execution timing

Used when price discipline is prioritized.

Execution certainty and price certainty rarely coexist.

Liquidity Depth and Execution Quality

Liquidity depth describes how much money exists across nearby price levels.

Deep Market Example

Major football match close to kickoff:

| Price | Available |

|---|---|

| 2.00 | €50,000 |

| 1.99 | €45,000 |

| 1.98 | €40,000 |

Large orders execute with minimal price change.

Slippage remains small.

Thin Market Example

Lower league event days before start:

| Price | Available |

|---|---|

| 2.00 | €200 |

| 1.98 | €150 |

| 1.94 | €120 |

Even moderate orders remove several levels instantly.

Slippage increases dramatically.

Liquidity determines execution stability.

Timing Risk and Market Competition

Exchange markets are competitive environments where multiple participants submit orders simultaneously.

Between the moment a trader clicks and the order reaches the market:

- other traders may consume liquidity,

- automated strategies may react faster,

- prices may already move.

Slippage often reflects competition speed rather than incorrect pricing.

Latency matters.

Volatility and Slippage

Slippage becomes more frequent during periods of rapid price movement.

Common high-volatility moments include:

- team news announcements,

- injury confirmations,

- red cards,

- late match situations,

- event start transitions.

During volatility, liquidity constantly relocates.

Displayed prices may disappear before execution completes.

Partial Matching and Average Price

Exchange orders are frequently matched in multiple fragments.

Instead of a single execution price, traders receive an average matched price calculated across all fills.

Example:

- €300 matched at 2.00

- €400 matched at 1.99

- €300 matched at 1.97

Average matched odds ≈ 1.986

Understanding average execution is essential when evaluating performance.

Hidden Cost of Slippage

Slippage represents an indirect trading cost.

Even with low commission rates, repeated slippage reduces long-term profitability.

Two traders paying identical commission may achieve different results solely due to execution quality.

Execution efficiency becomes a competitive advantage.

Managing Slippage Risk

While slippage cannot be eliminated entirely, it can be managed.

Common approaches include:

- trading in high-liquidity markets,

- splitting large orders,

- using limit prices,

- avoiding volatile moments,

- monitoring market depth before execution.

Professional participants manage execution risk as carefully as directional risk.

Slippage as a Structural Feature

Slippage is not a flaw of betting exchanges.

It is evidence of a live market where prices adjust dynamically according to supply, demand, and competition.

Perfect execution would imply a static market — which exchanges are not.

Understanding slippage transforms execution from uncertainty into measurable market behavior.

In exchange environments, price is only part of the trade.

Execution quality completes it.